Skip to content

Skip to content

Choosing life insurance can feel overwhelming. But it doesn’t have to be.

Let’s break down the three main types of life insurance — Term, Whole Life, and Universal Life (UL) — so you can see exactly how they work and which one fits your needs.

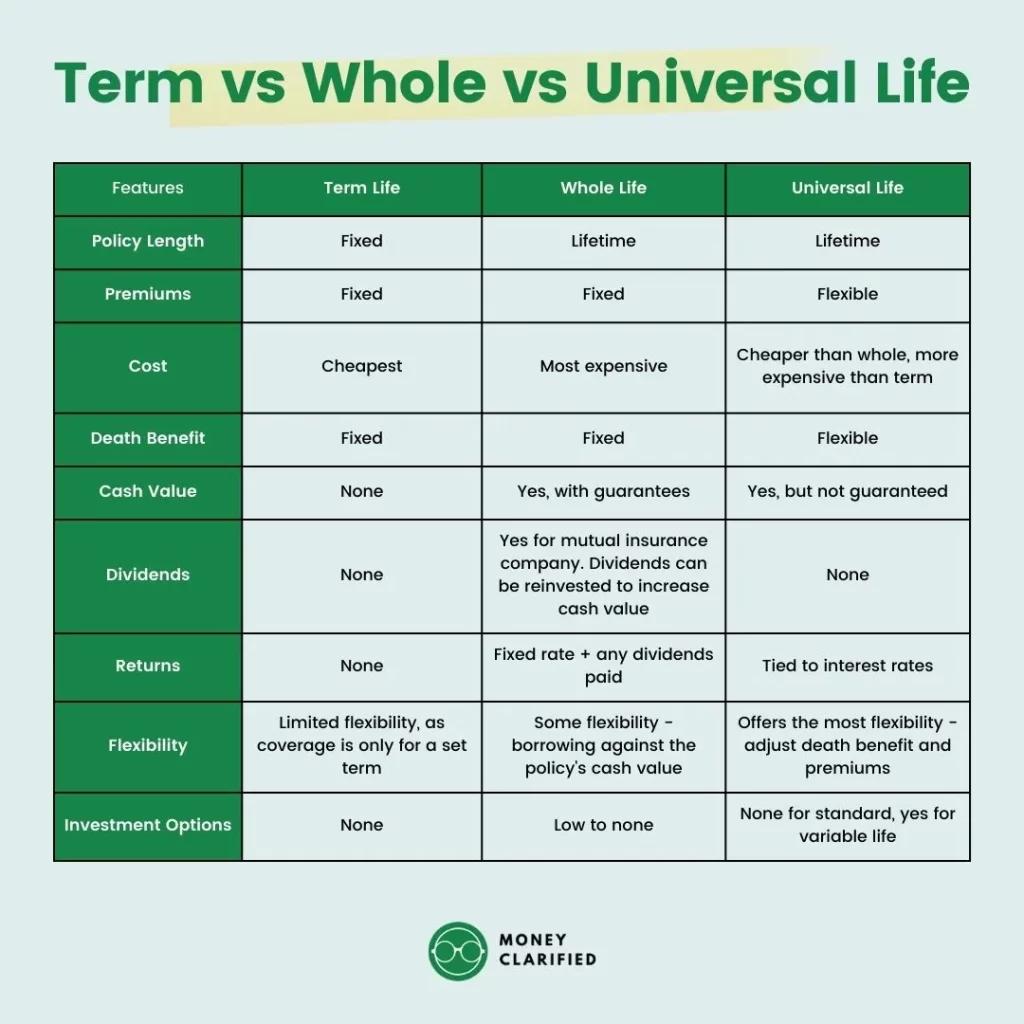

Quick Comparison

| Feature | Term Life | Whole Life | Universal Life (UL) |

|---|---|---|---|

| Coverage Length | Set term (10–30 yrs) | Lifetime | Flexible (can last decades or lifetime) |

| Cost | Lowest | Highest | Moderate |

| Cash Value | None | Guaranteed | Flexible growth |

| Flexibility | None | Fixed | Adjustable |

| Best For | Temporary protection | Long-term certainty | Flexibility + living benefits |

Term Life Insurance

Simple. Affordable. Temporary.

Term life is designed to cover a specific window of risk — like your mortgage, income replacement, or raising kids.

Best for:

– Mortgage protection

– Young families on a budget

– Income replacement (10–30 years)

Pros:

– Lowest cost

– High coverage amounts

– Easy to understand

Cons:

– Expires

– No cash value

– Rates increase if you renew later

Think of term as “renting” coverage.

Whole Life Insurance

Permanent coverage with guarantees

Whole life is built for lifetime protection and stability. It includes a guaranteed cash value that grows over time.

Best for:

– Final expense planning

– Estate planning

– People who want certainty and fixed structure

Pros:

– Never expires

– Fixed premium

– Guaranteed cash value growth

Cons:

– Higher cost

– Less flexibility

– Slower growth vs. other options

Think of whole life as “owning” a fully guaranteed policy.

Universal Life Insurance (UL)

Flexible, customizable, and strategic

Universal life is the middle ground — it gives you permanent coverage with flexibility in premiums and death benefit, plus cash value growth potential.

Best for:

– Long-term protection with flexibility

– Mortgage + income protection hybrid strategies

– Clients who want living benefits + control

Pros:

– Adjustable premiums

– Cash value accumulation

– Can be structured for specific goals (e.g., 20–30 years coverage)

Cons:

– Requires proper design

– Performance can vary depending on structure

Think of UL as a “custom-built” policy.

Which One Should You Choose?

It comes down to your goal:

– Need maximum coverage for the lowest cost? → Term

– Want guaranteed lifetime protection? → Whole Life

– Want flexibility + long-term strategy? → Universal Life

Pro Tip (What Most People Don’t Know)

You don’t have to pick just one.

Many of our clients use a blend strategy, such as:

– Term for maximum protection

– Universal Life for long-term flexibility and living benefits

This creates strong coverage today + financial options later.

Next Step

Before we finalize anything, we need to complete the qualification step to see what you actually qualify for based on health, age, and goals.

It only takes about 5–10 minutes.

Once we do that, we can structure the right plan and properly close out your file.

Ready to find your best fit? Let’s get started.

About DeFazio Insurance Brokerage

DeFazio Insurance Brokerage is an independent life insurance brokerage helping families compare coverage from multiple carriers. Whether you’re looking for term life insurance, mortgage protection, permanent life insurance, or living benefits, we help you find coverage that fits your goals and budget.

Andrew J. DeFazio

President | DeFazio Insurance Brokerage

(916) 964-7786

www.defazioinsurance.com

CA License #4437004

NPN #21436902