Skip to content

Skip to content

Most people hear “life insurance” and assume it all does the same thing.

It doesn’t.

There’s a big difference between general life insurance and a plan that’s specifically built to protect your home and your equity. If your mortgage is your largest expense—and your biggest asset—then how you protect it matters.

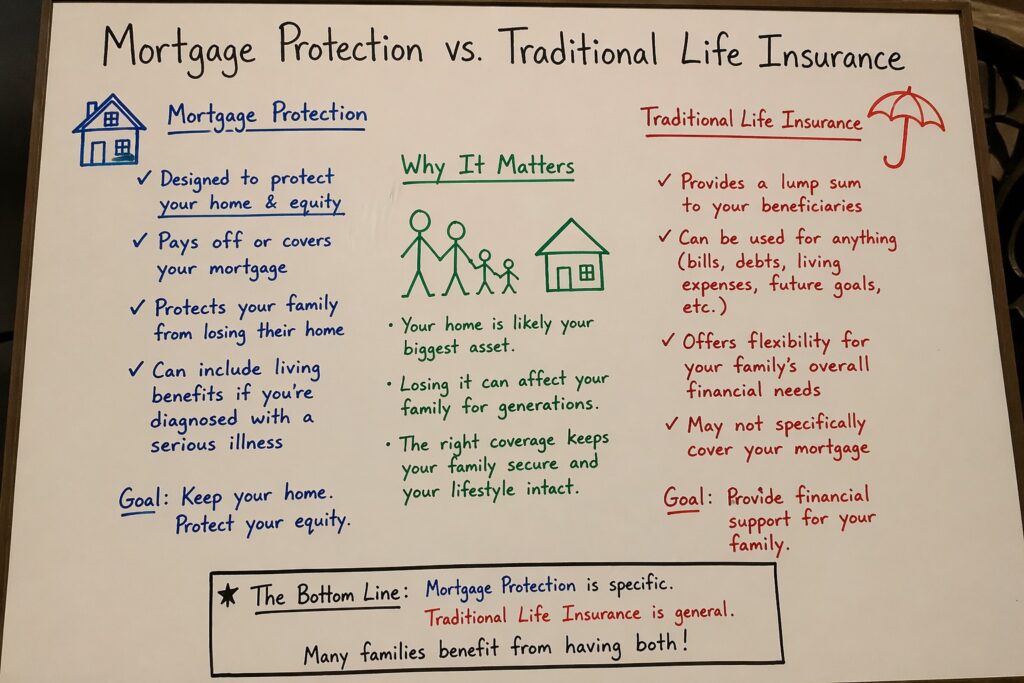

The Goal of Mortgage Protection

Mortgage protection is designed with one simple priority:

Make sure your home is not at risk if something happens to you.

If you pass away, become seriously ill, or lose income due to a health event, the policy is structured to provide funds that can:

- Pay off all or part of the mortgage

- Cover monthly payments during a difficult time

- Protect the equity you’ve built in your home

- Keep your family from being forced to sell

It’s not just about a payout—it’s about keeping your lifestyle intact.

Where Traditional Life Insurance Fits

Traditional life insurance is broader.

It’s designed to provide a lump sum that your family can use for anything:

- Income replacement

- Debt payoff

- Daily living expenses

- Future planning (college, retirement, etc.)

It’s flexible, but it’s not always focused.

Without a clear plan, that money can get spread across multiple needs—and your mortgage may not end up being fully protected.

The Key Difference: Purpose

This is where most people get it wrong.

- Traditional Life Insurance → General protection for your family

- Mortgage Protection → Targeted protection for your home

One is a wide safety net.

The other is a direct shield around your biggest liability and asset.

Why Mortgage Protection Matters More Than People Think

Your home isn’t just a place to live—it’s where your equity is built over time.

If something interrupts your income:

- Mortgage payments don’t stop

- Bills don’t pause

- And equity can disappear quickly if the home is lost

Mortgage protection is built to prevent that exact scenario.

Living Benefits: The Missing Piece

One of the biggest upgrades in modern mortgage protection plans is living benefits.

If you’re diagnosed with something serious like:

- Cancer

- Heart attack or stroke

- Chronic illness requiring care

You can access a portion (or all) of the policy while you’re still alive.

That means:

- You can keep making your mortgage payments

- You don’t have to drain savings or retirement

- You have time to recover without financial pressure

This is where many older or lower-tier policies fall short.

Do You Need Both?

In many cases—yes.

The strongest setup is often a combination strategy:

- A policy designed to protect your mortgage and equity

- Plus coverage that handles income replacement and long-term needs

That way, you’re not leaving your biggest asset exposed while trying to cover everything else.

Final Thoughts

Not all coverage is created equal—and not all policies are built with the same goal.

If your plan doesn’t clearly answer:

“What happens to my home if something happens to me?”

…then it may be worth taking a closer look.

Because at the end of the day, protecting your family also means protecting where they live.